Market Overview:

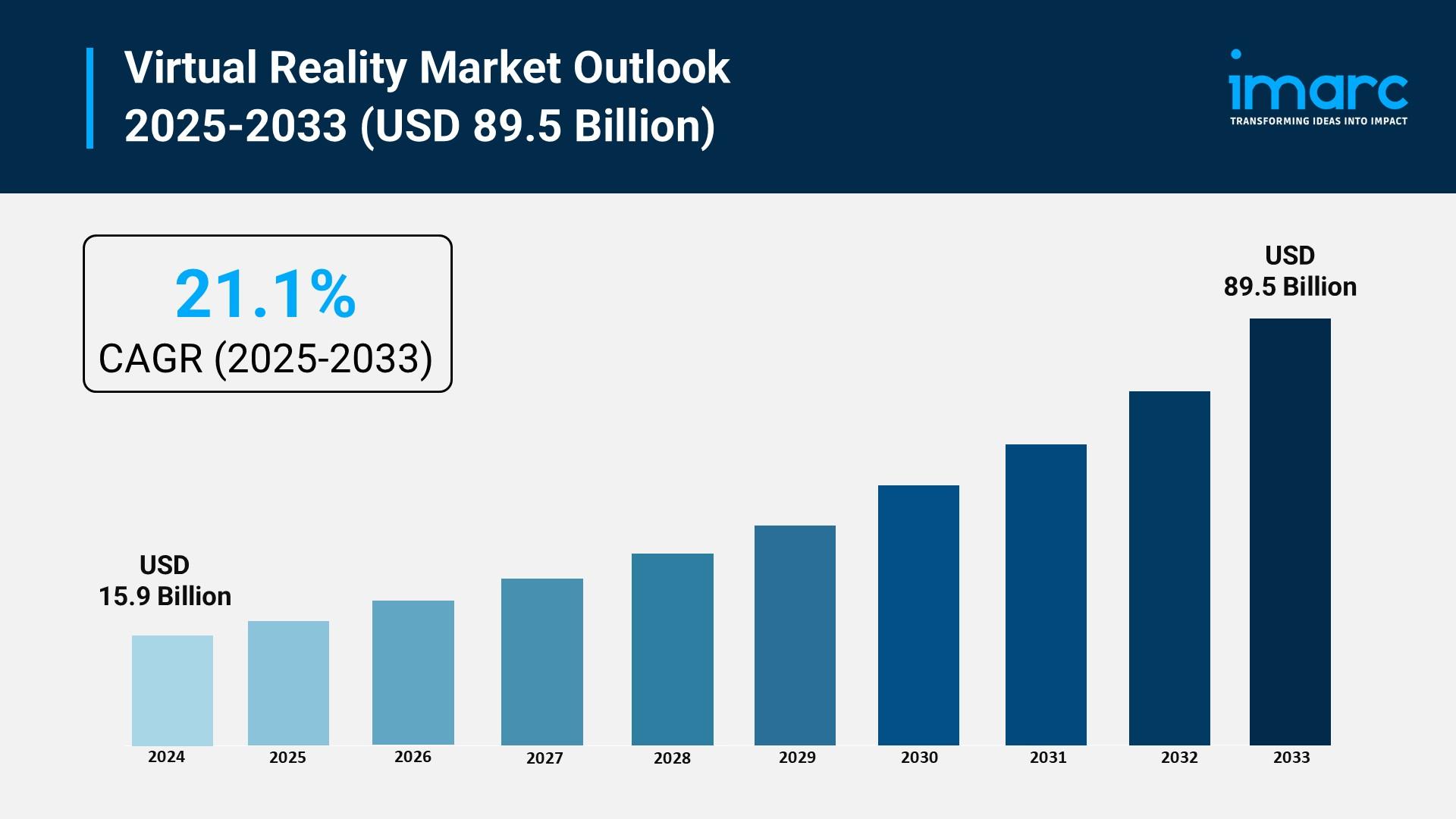

The virtual reality market is experiencing rapid growth, driven by enterprise adoption for training and simulation, continued advancements in hardware and accessibility, and expansion into healthcare and wellness applications. According to IMARC Group's latest research publication, "Virtual Reality Market Size, Share, Trends and Forecast by Device Type, Technology, Component, Application, and Region, 2025-2033", The global virtual reality industry size was valued at USD 15.9 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 89.5 Billion by 2033, exhibiting a CAGR of 21.1% from 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/virtual-reality-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Virtual Reality Market

- Enterprise Adoption for Training and Simulation

The commercial sector's increasing utilization of Virtual Reality for training, simulation, and design is a major growth factor. Large companies are leveraging fully immersive technology to recreate complex and hazardous environments for employee education. For instance, in the corporate training space, over 75% of Fortune 500 companies have integrated VR into their learning strategies. This includes major retailers using simulations for high-volume retail operations and the U.S. Army deploying VR for mental health modules. This transition is driven by the technology's ability to boost information retention by a reported 75% compared to passive methods, while simultaneously reducing travel and material costs associated with traditional training, making it a highly cost-effective solution for scaled workforce development across numerous industries.

- Continued Advancements in Hardware and Accessibility

Significant hardware innovations are driving consumer and commercial adoption by making devices more powerful, comfortable, and independent. The component market, specifically the hardware segment, currently accounts for the largest revenue share, reflecting continuous, heavy investment by major corporations. The increasing popularity of standalone Head-Mounted Displays (HMDs) is key, with these cable-free units capturing nearly half of the VR market revenue. Major tech players are continually releasing new generations of hardware that feature higher-resolution displays and integrated processing, improving the user experience and lowering the barrier to entry. This push for untethered, high-quality, and increasingly affordable devices is essential for widespread integration across both the consumer gaming and the professional environment.

- Expansion into Healthcare and Wellness Applications

The healthcare segment is emerging as one of the fastest-growing application areas for VR technology, showcasing high investment and regulatory validation. VR is being adopted for critical applications such as surgical training, where it allows medical professionals to practice complex procedures in a zero-risk, virtual environment. Furthermore, its use is rapidly expanding into therapeutic applications, including pain management, rehabilitation, and mental health. Regulatory bodies in key markets, such as the FDA, have begun granting approvals for VR-based mental health therapies and surgical training tools, which significantly validates the clinical efficacy and drives higher spending in this vertical. This clinical acceptance is boosting the segment, which is poised to be one of the quickest growing end-user markets.

Key Trends in the Virtual Reality Market

- Integration of Artificial Intelligence (AI)

A critical emerging trend is the seamless integration of AI and machine learning capabilities into the VR ecosystem. AI is enhancing VR experiences by enabling real-time personalization and the creation of highly responsive virtual environments. For example, AI-powered non-playable characters (NPCs) in simulations can react dynamically and realistically to user input, offering a level of interaction previously unattainable. This technology also significantly speeds up content development, with AI-powered tools allowing non-technical enterprise staff to build sophisticated training simulations within days. Furthermore, AI is crucial for optimizing the rendering process to deliver hyper-realistic visuals, even on lower-end devices, by employing techniques like foveated rendering based on real-time eye-tracking data.

- Emergence of 5G-Enabled Cloud and Edge VR

The deployment of 5G infrastructure is enabling a shift toward cloud-based and edge-computed VR experiences, eliminating the need for high-end local processing. This trend is driven by the ultra-low latency and high bandwidth of 5G, which permits complex graphical rendering to occur on remote servers and be streamed back to a lightweight, standalone headset. A concrete application is in Virtual Tourism and large-scale industrial collaborations, where massive 3D models of cities or factory floors can be accessed by multiple remote users without performance lag. This untethered, real-time streaming capability democratizes access to high-fidelity VR, allowing users in Asia-Pacific and other regions with rapid 5G rollout to engage in data-intensive virtual activities previously limited to users with expensive local hardware.

- Mixed Reality and the Continuum of Extended Reality (XR)

The market is moving beyond pure Virtual Reality into the broader category of Extended Reality (XR), where the line between AR and VR blurs into Mixed Reality (MR). This trend involves combining the full immersion of VR with the ability to see and interact with the real-world environment. A prime example is the use of high-end headsets that offer pass-through technology, allowing users to overlay digital twins or design blueprints directly onto a physical workspace. Manufacturers, such as car companies, are utilizing MR to test vehicle designs or assembly line optimizations by allowing engineers to interact with full-scale, virtual prototypes that are visually anchored within the physical factory. This ability to blend the virtual and real worlds enhances collaboration and operational efficiency by maintaining real-world context while leveraging 3D digital data.

Leading Companies Operating in the Global Virtual Reality Industry:

- CyberGlove Systems Inc.

- Eon Reality Inc.

- Google LLC (Alphabet Inc.)

- HTC Corporation

- Microsoft Corporation

- Oculus VR LLC (Facebook Inc.)

- Samsung Electronics Co. Ltd.

- Sixense Enterprises Inc.

- Sony Corporation

- StarVR Corp (Acer Inc.)

- Ultraleap Ltd.

- Unity Software Inc.

Virtual Reality Market Report Segmentation:

By Device Type:

- Head-Mounted Display

- Gesture-Tracking Device

- Projectors and Display Wall

HMDs dominate the market due to their immersive experiences and advancements in display technology across various industries.

By Technology:

- Semi and Fully Immersive

- Non-Immersive

This segment leads the market by providing engaging and interactive experiences through advanced hardware integration.

By Component:

- Hardware

- Software

Hardware is the largest segment, crucial for delivering immersive VR experiences with continuous innovations enhancing accessibility and performance.

By Application:

- Aerospace and Defense

- Consumer

- Commercial

- Enterprise

- Healthcare

- Others

The commercial sector holds the biggest market share, leveraging VR for enhanced customer engagement in retail, real estate, and entertainment.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America leads the market with over 37% share, driven by strong tech infrastructure, high adoption rates, and significant investments from major companies.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302